Let's look at the benefits of buying a home. Normally we just look at the dollars and cents. But there is so much more to owning a home.

Home ownership has been a dream of Americans for years. “Buying remains the more attractive option in the long term. As people get more savings in their pockets, buying becomes the better option.”

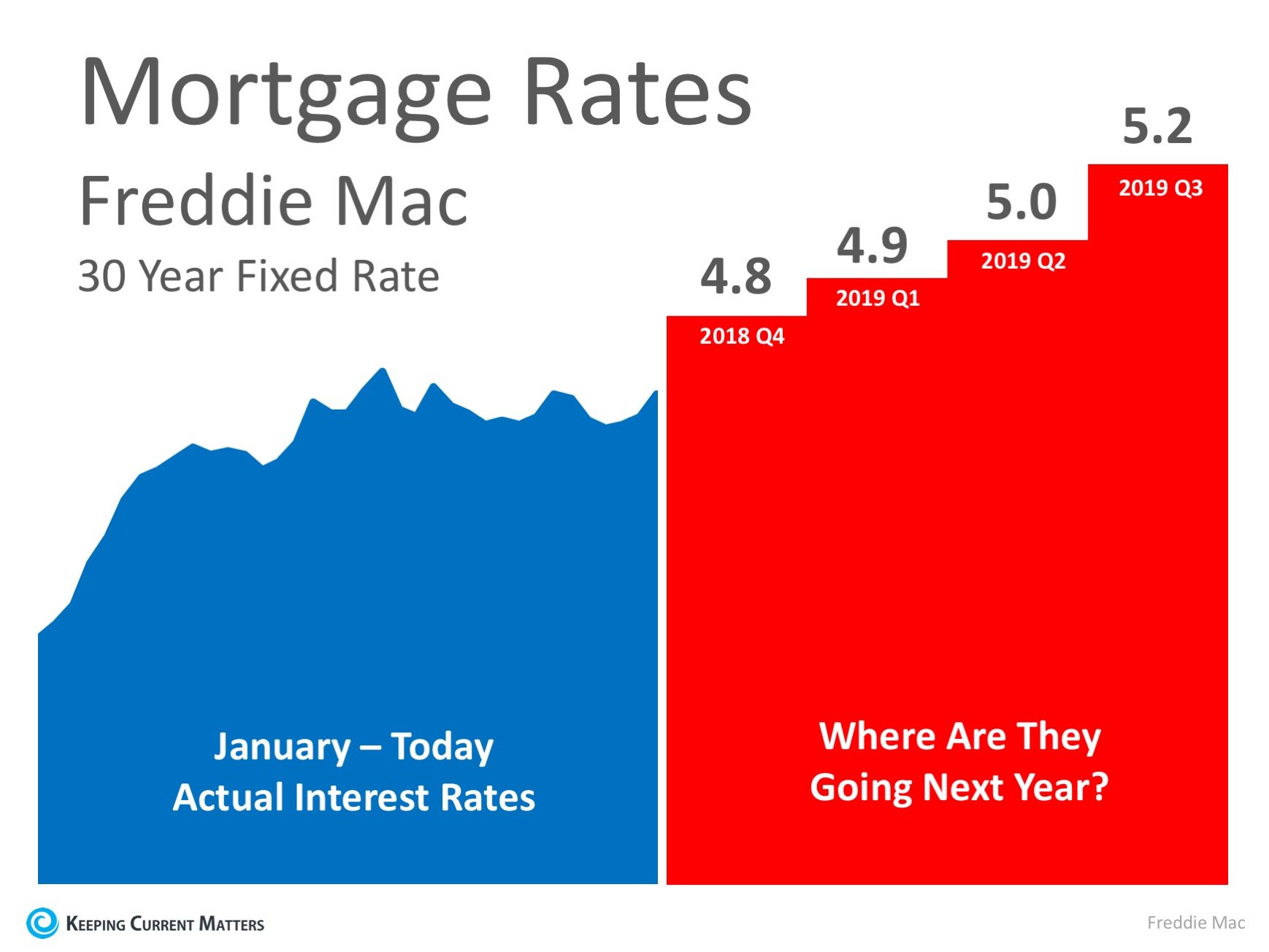

What proof exists that owning is financially better than renting?

1. In a previous blog, we highlighted the top 5 financial benefits of homeownership:

- Homeownership is a form of forced savings.

- Homeownership provides tax savings.

- Homeownership allows you to lock in your monthly housing cost.

- Buying a home is cheaper than renting.

- No other investment lets you live inside of it.

2. Studies have shown that a homeowner’s net worth is 44x greater than that of a renter.

3. Less than a month ago, we explained that a family that purchased an average-priced home at the beginning of 2018 could build more than $49,000 in family wealth over the next five years.

4. Some argue that renting eliminates the cost of taxes and home repairs, but every potential renter must realize that all the expenses the landlord incurs are already baked into the rent payment – along with a profit margin!

Bottom Line

Owning your home has many social and financial benefits that cannot be achieved by renting.